Land Tax in Queensland: A Look at the Literature

Source: The Conversation

Surveying what economists have written about land value taxation, with a focus on the Queensland context

A quick note before reading: this post is a survey of the academic and policy literature on land value taxation. Any views expressed are personal and don’t represent the views of my employer. Where reform options are discussed, they’re attributed to the authors and reviews that proposed them, not put forward as my own positions.

Introduction

Land tax (also called land value tax) sits in an unusual spot in tax policy. Surveys of economists tend to show strong support for it, while the general public is mostly dismissive or neutral, regardless of how much the housing crisis is in the news. This post tries to bridge that gap by walking through what the economics literature says about land value taxation, describing the design of the current Queensland (QLD) state land tax, and laying out the reform options that have been proposed, mostly by the Henry Tax Review.

Internationally, land tax is a policy with a long history of support among tax reformists and economists. In Australia, state and territory land taxes are in place nearly country-wide, with only the Northern Territory exempt. [1]

What is a Land Tax?

In general, a land tax is a tax on the unimproved value of land. Landowners pay a recurring tax on their land that doesn’t include the value of any buildings or other improvements. In a lot of other countries, property taxes are imposed instead, which fall on the combined value of land and improvements.

The literature commonly contrasts these two bases on the basis of incentive effects. Taxing improvements changes the marginal return to development, while taxing the unimproved value of land doesn’t. A survey by the Kent Clark Center reports that a majority of economists agree shifting the tax burden from improvements to land would enhance development incentives and boost economic activity. [2]

Empirical work has looked at this directly. Oates and Schwab (1997) studied Pittsburgh’s split-rate tax (which taxes land at a higher rate than improvements) and found that the shift toward taxing land was associated with more land development, less urban sprawl, and reduced land speculation. [3]

Besides the incentive story, the other big property associated with land tax in the literature is efficiency. The term sounds technical, but the intuition is pretty straightforward.

Efficiency of Land Tax

In public economics, efficiency in a single market refers to how well the quantity produced lines up with consumers’ willingness to pay for the good. Most taxes drive a wedge between the price consumers pay and the price producers receive, pushing the market away from this alignment and creating what economists call “deadweight loss”.

Note: To keep things simple I’m not incorporating externalities, the costs or benefits incurred by parties not directly involved in a transaction. These do matter in a full treatment and can in some cases (like a tax on cigarettes) actually increase efficiency.

For example, consider a tax on pencils (for some arbitrary reason):

- Pencils are a fairly typical good. When the price rises, firms are willing to produce more.

- The tax increases the price consumers pay, so quantity demanded falls.

- The tax also decreases the price producers receive, so quantity supplied falls.

- The tax burden falls on both producers and consumers, and quantity traded is lower than it would have been without the tax.

- The market is distorted, which is the deadweight loss mentioned above.

A tax on land works differently:

- Land is very different to typical goods. The aggregate quantity of land is fixed, since you can’t make more of it.

- A tax on the unimproved value of land doesn’t change the price consumers pay, so quantity demanded is unchanged.

- The tax does decrease the price received by landowners, but doesn’t change the quantity supplied.

- The tax burden falls entirely on landowners, who can’t adjust supply and so can’t pass any of the tax through to consumers.

- The market isn’t distorted. Revenue is raised without creating a deadweight loss.

This is the result that sits behind the long-running argument, traceable back at least to Henry George, that land value taxation is uniquely efficient among broad-based taxes.

The diagram below lets you see this directly. Start with an ordinary good — upward-sloping supply — and raise the tax: a deadweight-loss triangle opens up, because the tax discourages mutually beneficial trades. Now drag the supply elasticity toward zero (or hit “make supply ≈ fixed”). As supply approaches the vertical, fixed-quantity case of land, the triangle collapses to nothing and the entire burden shifts onto the seller. The deadweight loss scales with the square of the tax and shrinks as supply gets more inelastic, formally , where is the slope of supply.

The theoretical case is solid, but the IMF (2022) notes that direct empirical evidence of large efficiency gains is limited. [4] The literature puts this down to a few things, including how few jurisdictions actually use land value taxes, low statutory rates where they do exist, and design features like narrow bases or imperfect valuation that depart from the textbook ideal.

Equity of Land Tax

Equity is the other big component of tax policy analysis, dealing with the distributional effects of a tax. It typically gets split into vertical equity (fairness across taxpayers with different income or wealth) and horizontal equity (equal treatment of taxpayers in similar circumstances).

A tax is considered vertically progressive if the average tax rate rises with income, and regressive if it falls. Plummer (2010) looks at a switch from property tax to land tax within residential properties in the US, and finds the switch is more progressive than the property tax it replaced. However, the paper also finds substantial variation in effective tax rates among taxpayers in similar groups, which the author flags as a horizontal-equity concern. [5]

The Plummer study covers one switch. The IMF (2022) notes that whether a land tax ends up progressive or regressive depends on both the distribution of wealth and the composition of household portfolios. [6] If the share of household wealth held in housing falls as total wealth rises (a pattern observed in some datasets), a land tax can end up regressive in direct incidence terms.

The same paper notes that overall progressivity also depends on what’s done with the revenue. The IMF working paper presents modelling where a higher land tax is paired with income tax cuts or transfers to lower-income households, and finds the package can benefit low- and middle-income households on net while increasing the tax paid by high-income households.

The economic-rent framing helps here. Land tax falls on what economists call economic rents, payments to a factor of production above the amount needed to keep it in its current use. Economic rents arise for a few reasons, but for land the key one is fixed supply, which can be natural or generated by zoning restrictions on urban land. Because these rents accrue without productive effort on the landowner’s part, the literature commonly identifies them as a tax base that’s both efficient (since supply is inelastic) and arguably fair (since the rent is unearned in the sense above).

Land Tax in Australia

Land taxes have been around in Australia for a long time. A federal land tax was introduced in 1910 and abolished in 1952, and state and territory governments progressively brought in their own land taxes after that. [7] The literature attributes the move from federal to sub-national administration partly to administrative considerations, with the immobility of land meaning rate differences across jurisdictions have very low efficiency cost compared with mobile bases like labour or capital.

The Land Tax in Queensland

Queensland’s implementation has a few features worth describing in detail.

The taxable value of land in Queensland is determined by an annual valuation done by the State Valuation Service. The methodology differs by zoning. Rural land is valued on an unimproved value basis (just the land itself, with no improvements counted). Non-rural land (which doesn’t include rural-residential in the “rural” category) is valued on a site value basis, which includes improvements like clearing or earthworks that prepare the land for development. The rationale for site value is that these improvements have effectively merged with the land over time, since they’ve become permanent, don’t require maintenance, and for practical purposes are invisible once integrated. [8] [9]

Queensland used to value all land using unimproved value. The switch to site value for non-rural land followed recommendations in the Chalk Report (1989) and the Smith Report (1990), which cited improvements in accuracy and ease of valuation. [10]

The value base is meant to reflect the highest and best use of the land, meaning its value at its potential highest-value use, regardless of current use. Mangioni (2014) observes that site value can achieve this where there are vacant land sales available for comparison, since vacant land trades at a price reflecting its highest and best use. [11] However, in highly urbanised locations where vacant land sales are rare, valuers have to use improved land sales adjusted to net out the value of improvements. Mangioni notes this adjustment process can be inaccurate where comparator improvements aren’t well-matched or where the location isn’t relevant, and that this in turn can compromise the highest-and-best-use principle. [12]

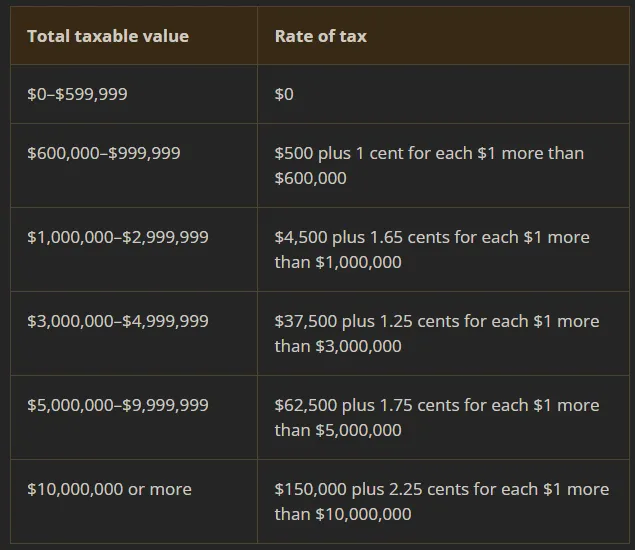

Moving to tax rates, the Queensland land tax has a progressive marginal structure. For an individual, the tax kicks in once the total taxable value of land owned exceeds $600,000, with marginal brackets above that threshold, as shown below:

Source: Queensland Revenue Office

A landowner’s primary place of residence is exempt from the tax. [13] The practical effect of this is that the tax applies to investment and commercial land above the threshold. The rates are also fairly low at the lower end of the schedule. An individual investor with total taxable land value of 1,300 a year. For land held by companies, the tax-free threshold is lower (only $350,000) and the marginal rates are significantly higher.

It’s also worth pointing out that local councils impose land taxes too, they’re just called “council rates”. [14] At least in Brisbane, the structure is broadly similar to the state land tax, but applies to owner-occupied homes as well as investment land, giving it a substantially broader base. [15]

In revenue terms, the Queensland land tax is smaller than its counterparts in other large states. ABC reporting in early 2024 noted that Queensland collects less than half the per-capita land tax revenue of New South Wales or Victoria. [16] In the 2022-23 budget, land tax raised 4.72 billion. [17]

Reform Proposals in the Literature

The Australia’s Future Tax System Review, commonly called the Henry Tax Review, was commissioned by the Rudd Government to guide tax reform and was led by then-Treasury Secretary Ken Henry. It made a number of recommendations on land taxation. The first three sections below summarise Henry Review recommendations; the fourth covers a proposal from Mangioni (2014). The framing here is descriptive: these are recommendations made by the cited authors, not endorsements on my part.

Henry Review: a broader base, including the primary place of residence

The Henry Review recommends that land tax be levied on as broad a base as possible. The argument set out in the AHURI report by Wood et al. (2012) is that unequal treatment between rental and owner-occupied land breaks the standard incidence result. Where land can be used for rental or owner-occupied housing, taxing only the former reduces the after-tax return on rental investment, which the AHURI authors model as producing higher rents in equilibrium. [18] Broadening the base, in the Henry Review’s framing, restores the textbook efficiency property.

The same AHURI paper also models the effect of a broader-based land tax on land values. Under their assumptions about capitalisation of expected future tax liabilities into prices, the average plot of land declines in real value by around 5%, rising to roughly 12% for land in and around the CBD. [19] The authors describe this estimate as conservative, since it doesn’t incorporate the additional house-price effect of phasing out stamp duty.

Henry Review: phase out stamp duty, with land tax revenue replacing it

The Henry Review recommends that stamp duty (transfer duty) be phased out over time, with the lost revenue replaced by an expanded land tax. A deep-dive into stamp duty is beyond the scope of this post, but the economic case set out in the Henry Review itself is that transfer duty discourages property transactions, which the review argues impedes the efficient allocation of housing to its highest-value occupants. The review also argues it imposes a higher effective tax burden on households who relocate more often, for reasons unrelated to ability to pay. [20]

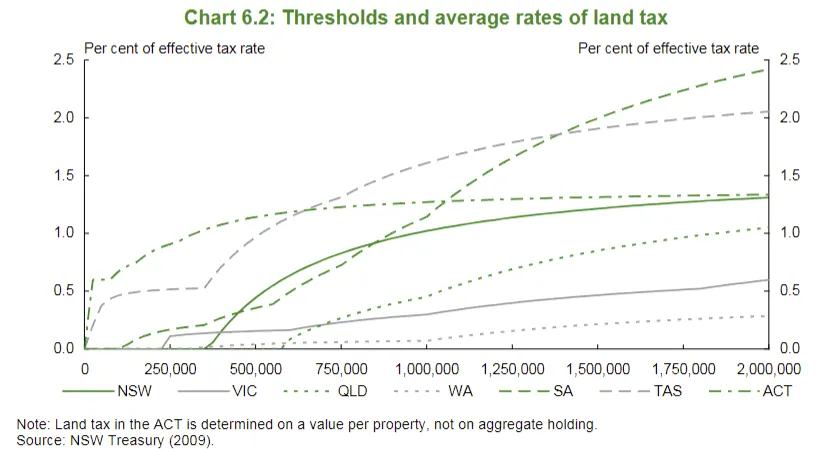

Mangioni (2018) notes that stamp duty revenue is large enough that immediate replacement isn’t feasible, and that the literature generally proposes a phased transition over 5 to 10 years. [21] The chart from the Henry Review below shows the headroom available in the existing structure. Even at the top of the bracket schedule, the effective rate is around 1% of land value.

Source: Henry Tax Review

Henry Review: per-square-metre value as the basis for marginal rates

The Henry Review recommends that rates be set on the per-square-metre value of land rather than on aggregate land holdings, with a tax-free threshold below which low-value land is exempt and progressive marginal rates above it. The argued advantage is that this base doesn’t depend on the identity of the owner or the use of the land, which avoids the distortions associated with aggregating holdings.

The AHURI study models the spatial consequences of various designs. [22] A fully broad-based land tax including agricultural land leaves the urban boundary and city density largely unchanged. A version that exempts agricultural land (the more politically common configuration) is found to reduce urban sprawl through higher density, smaller dwellings, and taller buildings, with shorter commute times but higher CBD house prices and rents. Comparing a progressive per-square-metre design against a flat-rate alternative, the same study finds the progressive design concentrates the burden on relatively affluent suburbs near the CBD where land values are highest.

Mangioni (2014): moving to Capital Improved Value

Mangioni (2014) proposes shifting the valuation base from site value to Capital Improved Value (CIV). [23] The proposal responds to the valuation difficulties noted earlier, where in dense urban areas with few vacant land sales, site value relies on adjusted improved-sales data that can mis-measure the highest-and-best-use value.

CIV combines two components: site value, and the added value of improvements. It can be administered either as a combined base or as a split-rate tax with a higher rate on the site-value component (since site value is the inelastically supplied part). Mangioni argues that valuing improvements at their highest-and-best-use level, drawing on sales of recently completed comparable developments, anchors the base to current market reality. He also argues this preserves the incentive properties of land taxation by ensuring that an individual landowner’s improvement decisions don’t change their tax burden. [24]

Closing Observations

The economic literature on land value taxation is fairly consistent on a few descriptive points. The inelastic supply of land underpins a strong theoretical efficiency result. The distributional effects of any specific design depend on wealth composition and the use of the revenue. Australian sub-national administration has practical advantages given the immobility of land. The reform proposals from the Henry Review and the subsequent academic literature represent one set of design options that follow from this analysis. How (and whether) any such reforms are implemented is a matter for elected governments, weighing economic considerations alongside political, distributional, and administrative factors that fall outside the scope of this survey.

References and links above are preserved from the version of this post that surveyed this literature in 2024. Where empirical figures (such as revenue collections or rate schedules) are quoted, they reflect the data available at that time.